Highlights

Key Takeaways

- STOCKS: Markets Price in “Economic Nirvana”

- Based on Valuations, Cyclical Sectors Poised to Outperform

- Oil Market Update

- Special Reports and Editorial: What the Fed Decision Means for Markets

Stocks

“Stocks rallied to fresh multi-month highs last week thanks to a further decline in CPI and PPI that increased Immaculate Disinflation hopes that helped markets ignore a hawkish dot plot from the Fed.”

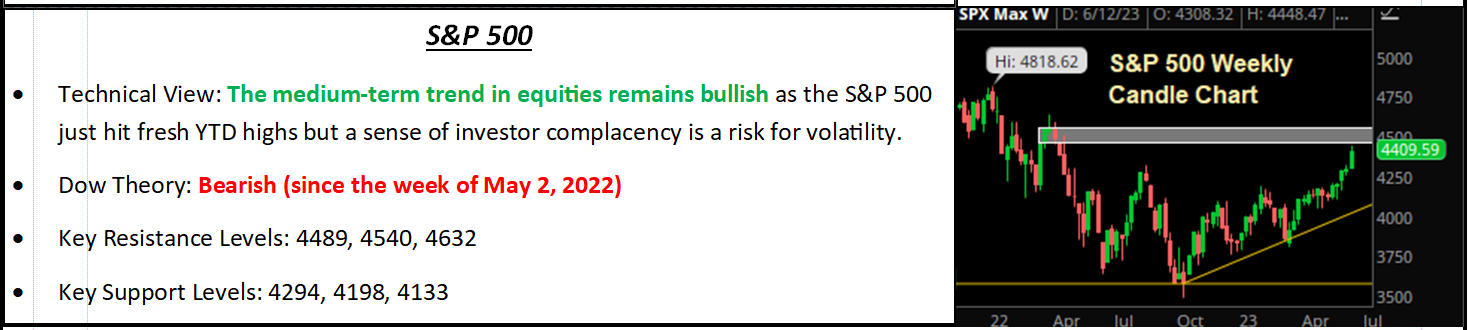

S&P 500

The S&P 500 reached 4,400 and came very close to our “best case” scenario target, as further declines in CPI/PPI combined with stable economic data to offset a Fed that, if economic data does not change, plans to hike an additional 50 bps by year-end.

Currently at 4,400, the market is trading on an 18.3X valuation, which given the macroeconomic reality is about as “best case” as one can get. That said, bullish momentum and chasing can continue to push the S&P 500 higher from here, but at these levels (and above) it is important to realize that stocks are reflecting a future economic and market “nirvana” where 1) Immaculate disinflation occurs, 2) Growth remains solid and 3) 2024 S&P 500 earnings expectations of $240 not only stays solid, but actually rises.

Anything is obviously possible, and it is entirely true the market and economy have performed better than most expected (including our investment team), but at 4,400 the S&P 500 is aggressively pricing in a lot of good things occurring, and virtually zero negative surprises.

Now, to be clear, we are trying not to sound like a perma-bear, because we are not. We are long stocks (albeit primarily defensive sectors and holding a large cash position given our general cautious outlook, so we are participating in the rally but relatively underperforming the benchmarks). We do not enjoy consistently warning of risks to the markets when 1) Those risks don’t materialize in the near term or 2) When the market ignores those risks. But we do view it as one of our jobs to make sure you understand the other side of sentiment. That was true when stocks were dropping hard in 2022 and many analysts became more negative than the facts implied, and it is true now when, suddenly, many analysts that were bearish to start the year are upping price targets.

The truth is the outlook for the economy and stocks is more balanced than the price action would imply. On a macro level, the economy is just now starting to feel the impact of 500 bps of rate hikes. Yes, a recession hasn’t started yet. Yes, it’s possible the economy doesn’t slow. However, that is not what history implies will happen. It is also not what the bond market has been saying, incredibly consistently, for the past year. Finally, while those signals have not yet been correct, our investment team highly believes they still warrant consideration.

On a micro level, corporate America is facing a more challenging environment. The margin expansion that inflation gave companies will partially reverse as disinflation takes hold. Meanwhile, there has been no economic slowing to impact earnings yet—as it is just starting now.

Bottom Line

We are happy the S&P 500 is at 4,400. We hope it keeps going. Bull markets are better for everyone in our business than bear markets. However, our job is to stay focused on facts and ensure you understand them as they are, not as we hope them to be. That is why we will continue to talk about risks to this market, and defend our current positioning, because those risks are real.

Economic Data

What You Need to Know in Plain English

There were only two notable economic reports last week and both implied a clearly slowing economy (and more Economic data last week was mostly Goldilocks and that offset the hawkish FOMC “pause” for one simple reason: Investors know the data will dictate future Fed policy, not the “dots,” and the data last week showed a further decline in inflation (disinflation) and stable enough economic growth.

Starting with inflation data, both CPI and PPI showed further disinflation. Headline CPI declined to 4.0% y/y vs. (E) 4.1%, but more importantly the “super core” CPI (which is CPI less housing) dropped to 4.6% from 5.3%, and the Fed will welcome that as a positive sign that consumer driven inflation is declining. Similarly, PPI dropped to 1.1%, confirming that goods inflation also continues to ease.

Now, none of these numbers are where the Fed wants them, but they don’t have to be for the markets. Instead, the data just has to not refute the market’s expectation that disinflation is accelerating, and last week’s inflation data was good enough to further that expectation, and again that’s why the markets largely ignored the more hawkish dots.

Turning to growth data, virtually all the notable reports came on Thursday and while they weren’t “great” in an absolute sense, they did point more to a soft landing than a hard landing.

Retail sales were slightly better than expected on the headline and solid in the details (including the “control” group) and while not especially strong reports, they implied the consumer remains largely healthy. The first data points for June, Empire and Philly manufacturing, were both better than expected and Empire turned positive, while Philly was still modestly negative but both well off the recent lows. Now, these surveys are volatile and that has especially been true this year, but overall they show that economic activity did not suddenly drop so far in June.

The only “soft” reading last week was the weekly jobless claims number, which remained elevated at 261k. That’s not a “bad” number historically speaking and remains the shining example of economic resilience; but it does point to some potential softening in the labor market, and if that gets worse quickly (say a quick move towards 300k over the coming weeks) that will increase hard landing worries, but for now the labor market remains generally tight.

Bottom Line

Investors have embraced the positive scenario: That disinflation accelerates and declines enough that the Fed will not need to raise rates much higher than current levels, and that the economy will enjoy a soft landing. To be clear, the economic data does not confirm that will occur, but it did not do anything to damage that expectation, either, and stocks rallied as a result.

Commodities, Currencies & Bonds

“Commodities surged on a weaker US dollar and on Chinese growth expectations as officials announced more stimulus measures.”

Commodities traded with a risk-on bias last week as oil and industrial metals posted gains while gold declined amid rising optimism of a soft landing after the Fed’s “hawkish skip” was largely shrugged off with market-based rate hike expectations deviating notably from the FOMC’s latest dot plot. Natural gas notably rallied over 15% on the week to end at a one-month high.

Starting with energy, oil prices fell sharply to start last week as GS analysts abandoned their previously bullish call on oil and the refined products for 2023, lowering their year-end price target. That soured sentiment and sent both major crude benchmarks down by 4% or more on Monday. The price action improved from there, however, with still-strong consumer demand readings in the weekly EIA data combined with the “dovish doubts” about the Fed’s policy plans, which reinforced optimism for a soft landing in 2023.

For the fourth time this year, WTI held above key range support at $67/barrel and the American benchmark ended the week higher by 1.89%. Looking ahead, a continued rise with other risk assets amid soft-landing hopes is possible for the oil market, but a move beyond resistance in the low $80s near the 2023 highs is unlikely as it is rather difficult to make a convicted bull case for the quarters ahead as the deeply inverted yield curve continues to flash a historically accurate signal that the economy is on the brink of recession.

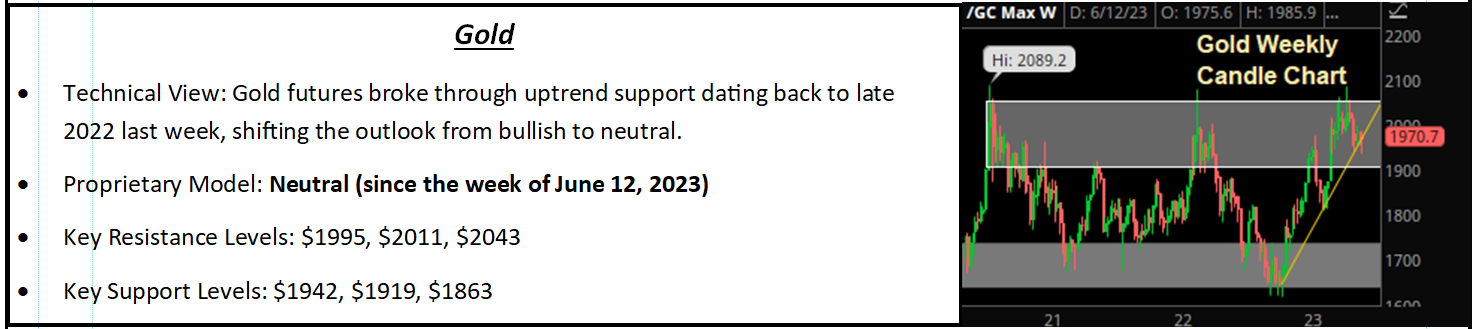

Gold

Turning to the metals, the new stimulus efforts by the Chinese government announced over the course of the week helped drive copper futures higher. Meanwhile, gold has not participated in the rally but rather declined amid rising Treasury yields as investors priced in a higher-for-longer Fed policy rate after the conclusion of the FOMC meeting. While industrials have enjoyed a solid rebound in recent weeks, copper is testing formidable resistance between $3.85 and $3.95, and a breakout higher, given the fundamentals, is unlikely while gold broke a long-standing uptrend last week shifting the outlook to neutral.

Bottom line for the metals, if we see the Dollar Index hold the 2023 lows and move higher, that will add renewed pressure to metals broadly.

Oil Market Update

EIA Data and Oil Market Update

The weekly EIA data revealed an outsized build in commercial crude oil stockpiles and larger-than-expected builds in the refined products. The details actually favored the bulls as demand metrics hit new multi-year highs.

Looking to the details, U.S. oil production held steady at 12.4MM b/d, a post-pandemic high, but the refinery utilization rate, which was expected to hold steady, dropped 2.1% to 93.7% last week. Lower refinery runs mean less near-term oil demand and that helps explain the sizeable build in crude inventories last week.

Bottom Line

Consumer gasoline demand remains strong and according to the latest data, it’s getting stronger as we start the summer driving season. That is a bullish influence for the broader energy market and in normal economic conditions, would be reason for rallying oil and refined product prices. But we are not in normal economic conditions and oil traders are looking at the macro picture with a still-aggressive Fed threatening the economy and an already deeply inverted Treasury yield curve forecasting a recession within the next few quarters. And the threat of a looming recession is the primary and controlling influence on the global oil markets right now, especially given that OPEC+ appears to be maxed out regarding their ability to support the market with output cuts at this time.

Special Reports and Editorial

What the Fed Decision Means for Markets

The Fed provided a hawkish surprise in the statement, and it caused some temporary declines in stocks, but the declines did not hold and the reason why is clear: The market does not believe the “dots,” and it shouldn’t. First, the dots have a very dubious track record of accuracy. Second, as we have said all year, it is not up to the Fed this year, it’s up to the data.

If inflation continues to decline and super core CPI falls closer to 4% and under 3%, then the Fed won’t hike twice between now and year-end. Or, if economic growth suddenly rolls over, the Fed won’t hike twice. Now, it’s entirely likely the Fed does hike once more, at the July meeting, but that is already largely expected from markets and as long as economic growth stays resilient, that will not be a material negative for stocks or bonds.

More broadly, think about this “Immaculate Disinflation” rally that has powered the S&P 500 close to 4,400. It has been driven by economic data: Inflation metrics have come down suddenly, while growth has stayed surprisingly resilient. As long as that stays the case, then it is not suddenly more likely that the Fed will hike rates twice by year-end. As such, we do not see the hawkish FOMC statement as a material negative, nor something that will derail the Immaculate Disinflation rally as long as growth stays solid and inflation metrics trend lower.

As to the question of “why” the dots show two additional rate hikes, we think the answer is because the Fed does not want its pause to further stoke inflation by investors taking this as a cue that they are “definitely” done and easing financial conditions. It is equivalent to a parent warning a child of the worst possible punishment so as to deter any possibly negative behavior.

Finally, we are not implying the market can simply ignore what the Fed says going forward. If inflation bounces back, and if growth remains hot, then the Fed would hike 50 bps between now and year-end. But that is conditional, and if inflation keeps falling and growth stays stable or slightly moderates, then the Fed will not hike another 50 bps, so the Fed commentary has to be taken in the context of economic data.

Second, long term the Fed is clearly pushing back very hard on the idea of rate cuts, and that means higher rates will strangle the economy longer than previously expected. That does raise the chances of an ultimate hard landing, although it is unlikely that is going to occur imminently.

Bottom Line

The key takeaways from the Fed are 1) Data remains the key to this market, 2) The risk of a recession and hard landing is not gone (nor is it very diminished) so we need to continue to watch for signs of that hard landing, because at these valuations a 10% decline on recession worries would just be the start.

By Vann Equity Management