Highlights

Key Takeaways

- Stocks: A Narrowing Path to an Economic Soft Landing

- Weekly Market Preview: All About Ukraine (Will there be a real cease fire?)

- Economic Data: Weekly Economic Preview: Inflation is key this week (CPI on Thursday)

- Special Reports and Editorial:

- It’s All About Escalation (And What Can Go Wrong)

- Why the SWIFT Ban and Other Sanctions Matter

- Update on Value/Growth Rotation

- Energy Update: OPEC+ Policy Decision and EIA Data

Weekly Market Preview: All About Ukraine (Will there be a real cease fire?)

Geopolitically, over the weekend there were attempts at localized cease fires in southern Ukraine to allow citizens to flee the cities, but those efforts have been, so far, a failure. More peace talks are scheduled for today although not much progress is expected.

Today there are no notable economic reports and no Fed speakers, so oil and geo-politics will continue to move markets. If oil continues to rally throughout the day, that will further pressure stocks and it’ll take meaningful progress on a cease fire to help markets rebound (and that doesn’t seem likely, at least not today).

Stocks

“Stocks dropped again last week as the Russia/Ukraine war further intensified, sending commodity prices soaring and increasing the chances of a future slow-down in economic growth. The longer the conflict goes on, the greater the headwind it will become on stocks.”

Near Term Stock Market Outlook: Neutral (SPHB: 50%, SPLV: 50%)

✓ What is Outperforming: Value and cyclical sectors have given back some of their early year outperformance in recent weeks, but as long as bond yields begin to rebound, value and cyclicals should outpace growth. RSP, XLI, XLV, XLP, XLF.

✓ What is Underperforming: Tech and growth stocks have recovered some ground on value recently but we continue to believe that progress in the economic recovery and subsequently higher interest rates will be a headwind for tech and a rotation from growth to value can be utilized to reduce tech overweights, but not abandon super-cap tech holdings altogether.

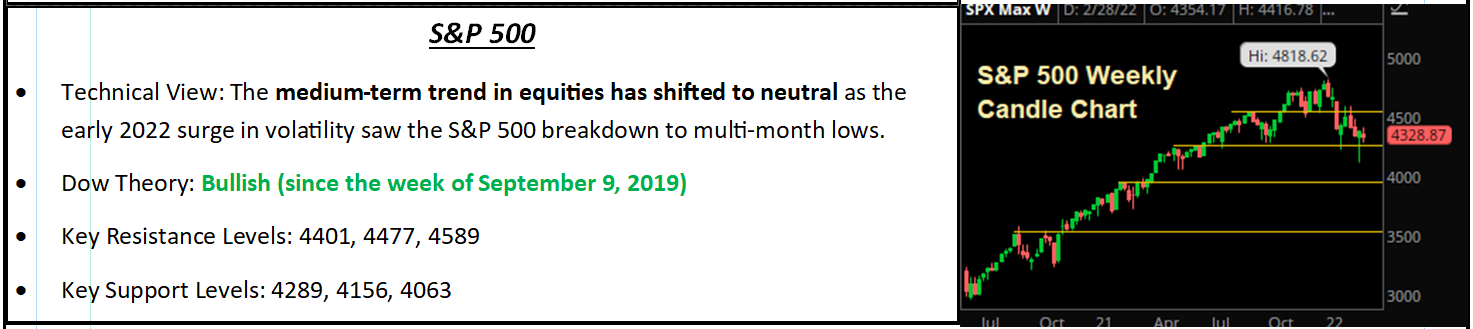

S&P 500

Narrowing the Path to a Soft Landing

When Russia invaded Ukraine approximately 10 days ago, we and other analysts highlighted that the duration of the conflict would be the key variable for markets—and more directly how long the conflict lasted, and how sustainably high it sent commodity prices, would determine whether the war was a material bearish influence.

At this point, the duration isn’t long enough yet to make us get materially more defensive, but it’s getting close. I say that because we aren’t even seeing de-escalation yet. We have a similar situation with inflation. Markets need inflation to recede, but before that happens it has to peak first (i.e. stop getting worse every month) and we’re not even there yet!

Relating it back to Russia/Ukraine, first, we have to get de-escalation. Then, we need a ceasefire that holds. Then, Russian troop withdrawals. Only after all of that will we see the historically crippling sanctions levied on Russia by the West begin to be removed—and at that point we should see a real decline in commodity prices. At this point, however, that’s potentially weeks away (if not longer) and that’s a growing problem for risk assets.

Meanwhile, the Fed remains on track to hike rates into a strengthening headwind on the economy, e.g. high inflation and exploding commodity prices, and a natural slowing of demand as fiscal spending/stimulus fully exits the system. Taken altogether, we are not ready yet to abandon our 4,300-ish—4,600 trading range in the S&P 500—but we are getting nervous about downside risks.

Barring a NATO/Russia war (which thankfully remains unlikely) this conflict will be a temporary influence on markets. Whether temporary means weeks or a month or two, it won’t be as big an influence over the rest of 2022. Instead, the major issue for this bull market remains the Fed, and specifically whether the Fed can remove accommodation, tame inflation, and not kill the recovery.

“Before Russia/Ukraine: The Fed had little room for error with high inflation and a looming slowdown in growth. Now, Russia/Ukraine has made that job significantly difficult via exploding commodity prices, which at a minimum will reduce economic demand and put more of a headwind on the economy over the coming months.”

As stated, we still view the S&P 500 in the 4,300-4,600 range. That said, until there’s de-escalation, we view this market as a “Hold” and will continue to audit our holdings to ensure we are overweight: 1) Low valuations and even some super-cap tech such as MSFT/CSCO/ORCL etc., and 2) Low volatility. We are not abandoning our call on cyclicals, and if banks/financials continue to get pummeled, we will look to selectively buy on “air pocket” days in the markets. However, at this point downside risks are building and while we still think the market can weather this geopolitical storm, we have got to see signs of geopolitical progress, otherwise the pressure on risk assets will grow and support between 4,200-4,300 will be broken.

Economic Data

What You Need to Know in Plain English

Need to Know Econ from Last Week

With commodity prices (oil) surging to multi-year highs in response to the Russia/Ukraine war, analysts are becoming nervous about near-term economic growth, although positively most of last week’s data was solid and, for now, the U.S. economy remains on solid footing.

The key report last week was Friday’s jobs report, and it hit our “Just Right” range. The job adds number was strong at 678k vs. (E) 399k, but the unemployment rate was 3.8% (above our 3.7% “Too Hot” designation) and wages were the big surprise coming in flat month over month (vs. (E) 0.5%) and rose 5.1% year over year (vs. a 5.8% expectation). That soft data helped the jobs report land firmly in Goldilocks territory, and it provided some brief relief from the geopolitical-driven losses.

Other data last week was similarly solid, if unspectacular. The February ISM Manufacturing PMI hit 58.6 vs. (E) 58.0 while New Orders rose 3.8 points to 61.7. Those are solid readings and don’t imply an imminent slowing of activity in the manufacturing space. The ISM Services PMI was a disappointment at 56.5 vs. (E) 60.9, while New Orders declined 5.6 points to 56.1, but while an underwhelming reading, some of that weakness could have been weather or Omicron related, and it’s still a reading that’s solidly in expansion territory (above 50).

Bottom line, with inflation high, commodity prices surging and the Fed about to start hiking rates, the markets need solid economic growth and they largely got it last week. However, sensitivity to economic data will rise over the coming weeks as the economy is now facing multiple short-term headwinds; and if data starts to roll over, that will be a new and material headwind on stocks as stagflation risks will surge. So, we will be watching the data very closely in the weeks and months ahead, because if stagflation is coming, we will want to get defensive quickly.

Powell gave his semi-annual testimony to Congress last week and it didn’t contain any material surprises, although he did voice his support for a 25-basis-point rate hike in March (vs. 50 bps) and Friday’s jobs report likely confirmed that’s what we’ll get (barring a huge surge in CPI this Thursday). We are getting closer to learning how quickly the Fed will hike rates (we get new “dots” at next week’s meeting) and that will provide some important clarity to markets—although that won’t be the positive it otherwise could have been unless we get de-escalation in Ukraine.

Important Economic Data This Week

The key report this week is Thursday’s CPI, and the key here is clear: It has to stop going up every month! That may seem simplistic, but year-over-year CPI has been moving relentlessly higher each month, and for anxiety about inflation to ease, we need to see the acceleration stop. Now, exploding commodity prices will obviously impact future CPI reports, but in the meantime, it will be helpful if we see some signs of a peak in CPI prior to that impact, so again the key for this report is to see hints that inflation pressures are peaking. From a Fed standpoint, this would have to be a very, very high number to get the Fed to hike 50 bps next week given Powell’s comments last week and the Goldilocks jobs report, although if CPI prints well above 8%, do not be surprised if a 50-bps hike is back on the table.

The other notable inflation indicator this week is the University of Michigan Inflation Expectations Index, and again that’s important because if consumer inflation expectations continue to rise, that will only further the Fed’s resolve to quickly remove accommodation, so we’ll be watching next Friday’s report closely. Bottom line, this week is all about inflation, and if it can give some hints of peaking, that could be a welcomed tailwind for stocks heading into next week’s Fed meeting.

Commodities, Currencies & Bonds

“Commodities exploded higher as the Russia/Ukraine war intensified and global commodity prices surged on general uncertainty and potential supply concerns.”

It was another historic week in commodities as oil prices surged into triple digits amid escalations in the Russia/Ukraine conflict, gold rallied on continued inflation concerns and copper spiked to records on renewed supply worries. The commodity ETF, DBC, surged by an unprecedented 14.98% on the week.

Oil prices were the focus within commodities last week as both WTI and Brent futures surged beyond $100/barrel. WTI ended the week higher by a staggering 25.08% at the highest level since 2008. The initial leg of the rally followed OPEC+ decision to raise production by just +400K b/d, sticking with their predetermined plan that preceded the Russia/Ukraine conflict; a topic they barely even noted in their release. Regarding Russia/Ukraine, the conflict continued to escalate over the course of the week despite diplomatic efforts aimed at reaching a ceasefire, meaning sanctions will remain in place for the time being while inventory data was bullish and previously promising prospects of an Iran nuclear deal faded.

Bottom line, just about every influence on oil, from geopolitics to storage levels, to demand, are all decidedly bullish for energy at the moment leaving the path of least resistance still higher with $125/barrel a distinct possibility in the weeks ahead. But to answer the question: what could cause oil to peak? It would have to start with the de-escalation of the Russia/Ukraine conflict including a timeline for sanctions to be removed and Russian oil being permitted back into the global market. Additionally, further progress towards an Iran nuclear deal would further ease concerns about the currently very tight global oil market.

Looking to metals, copper rallied to new record highs last week with a gain of 9.62% thanks to supply disruptions due to the Ukraine conflict and data that showed lower-than-expected production at the start of the year. From a demand standpoint, strong manufacturing data and the solid BLS report further bolstered the outlook for industrial metals.

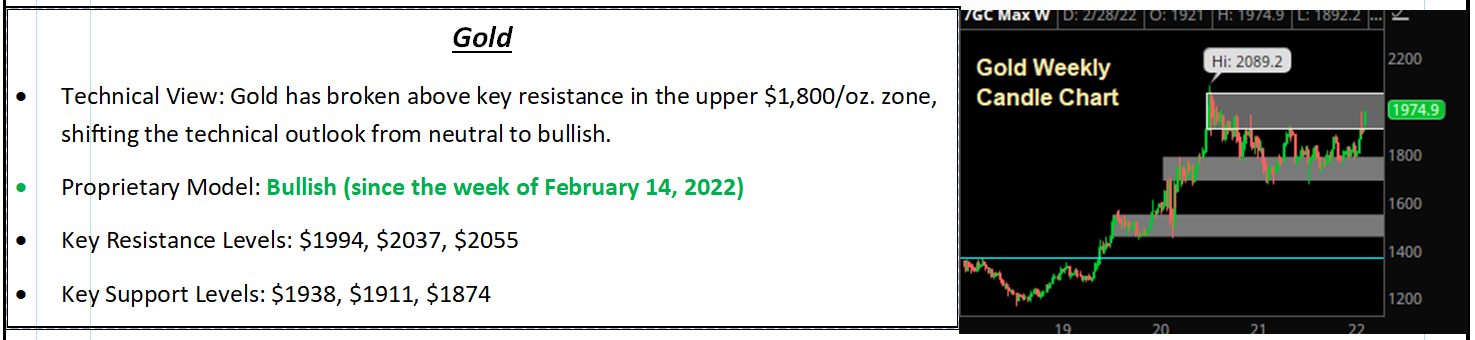

Gold

Switching to precious metals, gold rallied 4.49% on the week as inflation expectations via 5-Yr breakevens blew out to fresh record highs. Ongoing concerns about price pressures and Fed policy expectations being dialed back slightly due to geopolitics are both strong tailwinds behind gold here.

10-Year T-Note Yield Futures

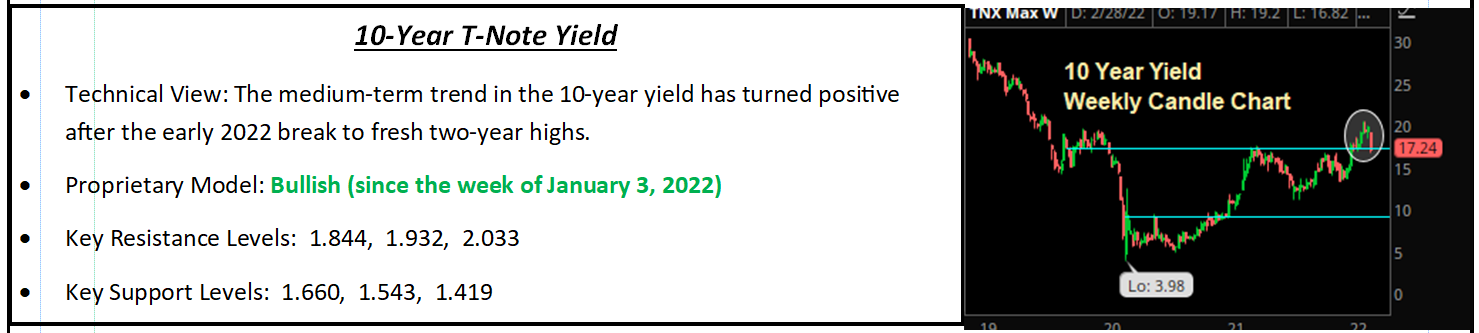

“The 10-year Treasury yield fell more than 20 basis points last week and the 10s-2s spread dropped to a fresh low of just 31 basis points as global bond markets are pricing in the increased chances of a broader economic slowdown, courtesy of Russia/Ukraine uncertainty and looming Fed rate hikes.”

In Treasuries, the risk-off move in markets pushed the 10-year yield sharply lower, as it fell more than 20 basis points below 1.80% on the continued escalation in Russia/Ukraine. Like the dollar, until there’s a de-escalation of hostilities, a ceasefire and sanctions relief, Treasury yields will remain under pressure near term. The combination of rising future growth fears, combined with Powell (and all Fed members) reiterating coming rate hikes, pushed the 10s-2s yield spread even lower as it broke below 30 bps in yet another ominous sign of potentially slowing future economic growth amidst rate hikes.

Bottom line, as we’ve said, the longer the Russia/Ukraine conflict continues, the bigger the headwind will be on the global economy, and we are seeing that now in real time, so again the sooner this situation de-escalates, the better.

Special Reports and Editorial

It’s All About Escalation (And What Can Go Wrong)

Stocks dropped last Tuesday despite solid economic data and the announcement of more peace talks, but that didn’t offset the reality that the situation in Ukraine is still escalating, and that means the sanctions on Russia also are escalating.

Russia has escalated the bombing of Ukraine as numerous videos of huge missile strikes in Ukrainian city centers showed, and that has resulted in mounting damage and civilian casualties. Beyond the obvious and most tragic consequence, which is of course the death and suffering of Ukrainian people along with the destruction of their country, this escalation also is having two additional negative consequences. First, it’s hardening the Ukrainian resistance, and second, it’s encouraging the West to escalate the sanctions on Russia.

Regarding the war, Russia may be trying to bomb Ukraine into submission, but if that’s the tactic then it may take a while and the ongoing peace talks likely won’t bear much fruit. That means a potentially longer conflict and a greater chance of a sustained commodity price spike that hurts the global recovery.

Regarding the West, Russia’s intensification of the attack on Ukraine has resulted in the intensification of Western sanctions on Russia, evidenced last week by British PMI Johnson pushing for more Russian banks to be banned from SWIFT, the STOXX delisting 61 Russian companies, and the U.S. not ruling out energy sanctions in the coming days if things don’t improve.

In sum, this is all additional escalation. We said at the onset of the attack that duration was the key—the longer it went on, the more negative it would be for markets because it’d continue to boost commodity prices (which is happening) and it’d become a stronger headwind on global growth (which is happening because of the sanctions).

So, what markets need is de-escalation, and we are getting the opposite. We are getting escalation from Russia who is stepping up a horrific bombing campaign and intensifying their assault, and we’re getting escalation from Ukraine who are stiffening their resistance and are unlikely to consider a truce while the country is being bombarded. And we are getting escalation from the West on sanctions. That’s increasing uncertainty, and it’s increasing the chances of contagion (financial, military or otherwise) and that’s why stocks are dropping again.

Positively, the sheer weight of the sanctions against Russia will likely prod them towards some sort of ceasefire in the coming days/weeks, so we do not see this as a bearish gamechanger (although clearly this remains a volatile and unpredictable situation).

Why the SWIFT Ban and Other Sanctions Matter

Some subscribers were a bit unclear why Russian banks being banned from SWIFT would cause fears of financial contagion, so I wanted to cover the topic briefly.

First, Russian banks being banned from SWIFT doesn’t mean they can’t complete international transactions. SWIFT just made international transactions easier, so those transactions will still occur, it’ll just take longer to move the money and be more complicated. That matters because Russia is a very interconnected country in Europe from an economic standpoint and injecting increased transaction times can potentially cause liquidity stress.

Here’s a basic example (all of this is made up). Let’s say a British bank gave a Russian company a short-term loan; and the Russian company banked through one of the banks now banned from SWIFT. Now let’s imagine that loan was supposed to be repaid yesterday. We don’t know what commitments that British bank had due that day—a day when it was counting on that money coming from Russia. The point being, if the British bank was counting on that money to fulfill another obligation, there is the possibility of a liquidity issue due to “slowing down” of Russian bank transactions.

Now, this is a very simplistic example but hopefully it illustrates this point: No economy that is as large or as interconnected with the global economy as Russia has ever been partially “cut off” from financing sources, had massive asset seizures, and been subject to being ejected from the global standard for quick and easy international money transfers. With a global economy built on leverage, no one is exactly sure where cracks might occur.

In all likelihood, this won’t be a problem (central banks will stand ready to provide emergency liquidity to anyone suffering from Russia’s partial ejection from SWIFT) but the point is we don’t know for sure, and that’s why these intense sanctions caused an uptick in anxiety last week. But to be clear, unless there is actual contagion, they should not be a headwind on stocks.

Update on Value/Growth Rotation

The Russia/Ukraine situation has essentially halted the rotation out of growth and into value, as financials, which are large weightings in value sectors, being hit by the dual headwinds of falling yields and sanction uncertainty. And that can continue as long as the Russia/Ukraine situation weighs on financials and other value sectors. Point being, don’t be surprised if tech/growth outperforms as the Russia/Ukraine situation evolves.

However, we don’t think this represents an end to the value outperformance because our value call is predicated on Fed tightening and continued multiple compression. Further, while the Russia/Ukraine situation can last several more weeks, the bottom line is that it will ultimately be temporary (a peace will be achieved sooner or later).

What is not temporary, however, is the Fed removing accommodation. While a lot of anticipated tightening is priced in, there remain risks to future growth that we think continue to favor value more broadly, and lower-multiple, high-quality earnings names.

Bottom line, we think tech/growth can outperform in the short term given the Russia/Ukraine uncertainty, but we would use that outperformance as another opportunity to lighten up on growth and allocate to value sectors to ensure a more balanced portfolio (or even mild overweight to value).

Oil Market Update

The recent price action in energy markets has been unprecedented and historic as the Russia/Ukraine conflict has fueled a fear bid across the oil and refined products complex, sending prices to multi-year, and in some regional markets, all-time highs. Energy prices first began to move higher last week after the March OPEC+ meeting concluded with members agreeing to stay on course and raise production by +400K b/d in April, despite the sanctions on Russia and sharp rise in prices in recent weeks. WTI prices are up more than 48% YTD while gasoline futures have rallied more than 25% just this week.

Looking through the weekly EIA data, the most notable piece of the release was that oil stockpiles at the hub in Cushing, OK, fell another million barrels to just 22.8 million barrels, which is approaching “tank bottoms” or the locations operational minimums which amplified an already panicky bid in front month oil contracts. Meanwhile, implied consumer demand for gasoline was little changed on the week at a solid 8.7MM b/d, refinery runs unexpectedly rose to 87.7%, and domestic production held steady at 11.6MM b/d, all bullish factors for the near-term outlook for oil prices.

News that delegations from both Ukraine and Russia were willing to continue ceasefire talks sparked a wave of risk-on money flows as traders bet on a potential de-escalation in the conflict and that saw oil prices pullback towards the flat mark in late-morning trade. But the broader energy markets bottomed and began to move methodically as it was increasingly apparent that Western sanctions on Russia were causing demand for Russian oil to completely disappear. That means in the near term, a roughly 6 million-b/d deeper deficit from wherever the physical market was coming into this conflict (that sent prompt calendar spreads of oil and refined products alike screaming higher). The six-month WTI spread notably blew out beyond $20/barrel to a new record level of backwardation. All of this likely led to margin calls into and through the settlement last week, which only amplified the moves.

Bottom line, the energy markets are in turmoil right now with a drastic supply and demand imbalance having emerged due to the sanctions on Russia. This will continue until there is a resolution to the conflict with Ukraine and the sanctions are ultimately removed. At this time, the market is “demanding” a ceasefire and unwind of sanctions with screaming oil prices and seeing a $125/barrel oil before the end of the week. That is by no means out of the question if there isn’t some degree of desolation. Having said all of that, the market is historically overbought on a low time frame basis and a likely violent unwind is looming but that would not change the fact that the physical market fundamentals continue to support higher prices.

By Vann Equity Management