Highlights

Key Takeaways

- Bottom Line: Real Focus Remains on the Fed and Growth

- Weekly Economic Cheat Sheet: Rising Threat of Stagflation?

- Is a Russian Invasion of Donbas a Bearish Game changer?

- Understanding Fed Hawks vs. Fed Doves

- FOMC Minutes Takeaways

-

EIA Data Takeaways and Oil Update

-

There are several economic reports due to be released today including: Case-Shiller Home Price Index (E: 1.1%), FHFA House Price Index (E: 1.0%), PMI Composite Flash (E: 51.9), and Consumer Confidence (E: 110.0). There is also one Fed speaker on the schedule: Bostic (3:30 p.m. ET).

- Russian President Putin recognized the independence of two “breakaway” regions in eastern Ukraine yesterday, but the risk of a full-scale invasion of Ukraine remains low.

- Regarding Ukraine, investors will await the announcement of new sanctions from the west against Russia and depending on how severe they are, it most likely will add to selling pressure on stocks today. Additionally, as of now, Secretary of State Anthony Blinken and his counterpart Sergey Lavrov are still scheduled to meet this week; however if the meeting is canceled it would suggest a more severe conflict is imminent, resulting in more risk-off money flows.

Stocks

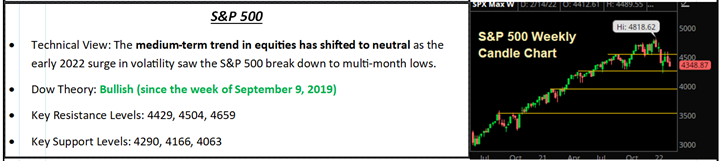

S&P 500

Last Week (Needed Context as We Start a New Week)

Equity markets remained volatile last week as investors eyed escalating geopolitical tensions surrounding Russia/Ukraine and digested mixed economic data ahead of monthly options expiration on Friday. The S&P 500 fell 1.58% on the week and is down 8.76% YTD.

Stocks began the week with a modest sell-off last Monday as simmering tensions between Russia and Ukraine weighed on sentiment while St. Louis Fed President Bullard reiterated his hawkish views on future rate hikes which sent the 2-year yield spiking by 10 basis points in early trade. Mixed geopolitical headlines saw the S&P hit new session lows in the afternoon before stabilizing into the close to end down a relatively modest 0.38%.

Equity markets snapped a three-day losing streak on Tuesday as news that Russian troops were returning from drills on the Ukrainian border to respective military bases helped ease concerns about a full-blown invasion. Those headlines helped offset another hot inflation report (PPI topped estimates) and mixed Empire State Manufacturing report that saw the S&P climb 1.58%.

On Wednesday, stocks opened lower after strong Retail Sales and Industrial Production data was perceived as hawkish ahead of the January Fed minutes release. The minutes were no more hawkish than feared and that paired with a quiet geopolitical backdrop saw the S&P 500 claw back to positive territory in afternoon trade, ending with a slight gain of 0.09%.

Volatility picked back up on Thursday as Russia accused Ukraine of shelling separatists in the breakaway region of Donetsk, which is very similar to how the annexation of Crimea began. President Biden once again reiterated that a Russian invasion of Ukraine was “imminent” and the S&P steadily dropped over the course of the day, ending down 2.12%.

Stocks wavered between gains and losses on Friday morning after it was reported that women and children were urged to evacuate the Donbas region of Ukraine amid escalating tensions while Putin reiterated that all military drills in the region were defensive and not provocative. Several Fed officials emphasized that the March rate hike will be 25 basis points and not 50, which helped stocks briefly turn positive in the afternoon, but the combination of geopolitical uncertainty and volatile money flows linked to options expiration saw the S&P 500 end down 0.72%.

Bottom Line

The Russia/Ukraine situation remains very fluid, tensions remain high, and in the short-term will remain a headwind on stocks. Specifically, over the weekend Biden continued to issue warnings that a Russian invasion was imminent, although a meeting between Secretary of State Blinken and Russia’s Sergei Lavrov is still scheduled to occur (as long as that’s going to occur an invasion remains unlikely).

The market has priced in at least some conflict between Russia and Ukraine; but a full-scale invasion of Ukraine remains unlikely. Instead, the more likely case is for Russia to do a repeat of Crimea and annex all or part of the Donbas region; which is precisely what President Putin did when he recognized the independence of the Donetsk and Luhansk over the weekend. Despite ominous media headlines, however, Russia recognizing the independence of those two regions and moving troops there, is not the type of invasion markets were fearing.

Looking forward, if the meeting between Blinken and Lavrov is cancelled, that would be a clear negative sign that a conflict is imminent and would continue to weigh on stocks until the full scope of the operation is known. While headlines surrounding Donetsk and Luhansk led to more volatility overnight, if the conflict ends here, that likely will cause a reflex rally, as stated previously this is not the invasion investors have been fearing.

So, the key questions for markets remain: How quickly will the Fed hike rates and, more importantly, how fast do they shrink the balance sheet? On growth, will we see a natural slowdown in the coming months, and if so, at what point does that get the Fed to be less hawkish?

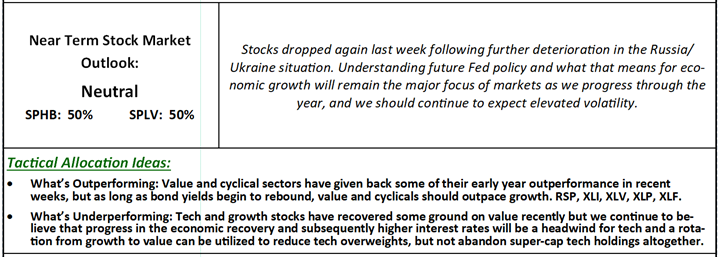

For now, we think the market has appropriately priced in Fed hawkishness and a mild slowing of growth, and that’s why we think the January lows can hold. As such, we continue to view any dip in the S&P 500 towards 4,300 (including this one) as a tactical buying opportunity for Value oriented strategies with low-volatility and cyclicals/commodities.

Conversely, we view 4,600 as a “ceiling” in this market until we have more clarity on the Fed’s plans for tightening, and we would use any relief rally towards that level to continue generating cash or to rotate out of tech and high-multiple growth stocks.

Bottom Line

Russia/Ukraine will continue to dominate markets in the short term and until there’s more clarity—but barring a major military conflict, we do not see that as breaking January lows (at least not sustainably).

Instead, the bigger impacts on this market remain Fed policy and economic growth. Those are the factors that ultimately decide whether the January lows are the bottom, or not. So, while we’re monitoring Russia/Ukraine, our main focus remains the Fed.

Economic Data

What You Need to Know in Plain English

Need to Know Econ from Last Week

Economic data was mixed last week while inflation pressures stayed firm, and while it’s too early to begin to worry about a whiff of stagflation, the data last week implies we could be seeing a slowing of activity and as a result we will be watching economic data much more closely in the coming weeks.

Last week gave us the first look at February economic activity, and it was underwhelming. The Empire Manufacturing Survey rose from January’s negative reading, but only to 3.1 vs. (E) 10.0. Meanwhile, the New Orders component also rose, but just to 1.4. Similarly, the Philly Fed Index also declined to 16.0 vs. (E) 19.7 while New Orders fell nearly 4 points to 14.2. Both numbers are terrible, and neither implies a material slowing of activity and the dip in activity is likely related to Omicron; but with the Fed so aggressive, there is little room for error from an economic growth standpoint. If these underwhelming readings are confirmed by today’s Flash PMIs, then we will see concerns start to rise about a loss of economic momentum.

Other data last week was better than the first look at February activity, as January Retail Sales rose 3.8% vs. (E) 2.0% while the “control” group, which is retail sales minus autos, gasoline and building materials, rose 4.8%. Those are obviously strong numbers, but they mostly just offset big declines in Retail Sales in December. Point being, they aren’t quite as good as they appeared. Industrial production also beat estimates, rising 1.4% vs. (E) 0.5%, although much of those gains were driven by a large increase in utility demand following a cold January.

Bottom Line

The data from January was solid, and it doesn’t imply at all that a slowdown is occurring; but again given Fed hawkishness there’s little room for error, so we will need to watch the data closely for any signs of a loss of momentum, because again that implies stagflation.

Finally, looking at last week’s FOMC minutes, they caused a mild rally not because they were dovish, but instead because they weren’t as hawkish as feared; and revealed nothing new on the policy front that changes the outlook for 75-100 basis points of rate hikes by June and balance sheet reduction (Quantitative Tightening) starting this summer. Looking forward, confirmation of the number of rate hikes and the QT plan will be the next major Fed catalysts, although we likely won’t get any material news on those fronts until March, via Powell’s semi-annual testimony to Congress and the March FOMC meeting.

Important Economic Data This Week

The two most important reports this week come today and Friday, via the February flash PMIs (out later this morning) and the Core PCE Price Index (out Friday). Of the two, the Core PCE Price Index is the more important report because inflation is the key variable for this market right now, and if that number again runs “Hot” like the January CPI did, then that will add to fears the Fed is going to get even more hawkish (and that will hit markets).

Today’s February flash PMIs are important also, because they are the first “big” number for February and markets will want to see stability in the data to ward off any stagflation fears. If the number is weak that will raise anxiety about a potential slowing of growth, which will just add to the headwind on this market.

Other notable data this week includes the revised Q4 GDP report (Thursday) but while that will get a lot of focus from the press, by now it’s a “stale” number as markets are focused on future growth, not what happened from October to December. We also get weekly jobless claims and New Home Sales (also on Thursday) but they likely won’t provide any surprises.

Bottom Line

This week’s data provides an opportunity to either increase stagflation worries or help ease those concerns, and the bulls will be looking for solid data and hints of a peak in inflation via the Core PCE Price Index. If we get that, and there is no Russia/Ukraine conflict, then stocks can rally. However, if the flash PMIs are underwhelming and, like the January CPI report, the core PCE Price Index implies inflation pressures are not easing, that will add another headwind on stocks and we should expect continued volatility.

Commodities, Currencies & Bonds

Commodities were mixed last week as improving prospects of a new Iran nuclear deal caused oil to sell-off despite the ongoing tensions between Ukraine and Russia, which fueled a fear bid in gold. Copper, meanwhile, traded relatively well given the cautious investor sentiment as economic data was mostly upbeat. The commodity ETF, DBC, edged up 0.30% on the week.

Energy has been in focus in recent weeks as tight fundamentals so far in 2022 have seen the global oil benchmark charge towards $100/barrel. The escalating tensions surrounding the Ukraine conflict further bolstered oil prices through the beginning of last week; however, the market focus shifted to Iran nuclear talks in Vienna where officials were said to be “as close as they have ever been to a deal.”

Such a deal would mean anywhere from 500K to 1MM bbls of crude hitting the global market in the coming months, which would be a bearish supply side development as that oil would more than compensate for the over-compliance by OPEC+ to their own production targets. It may even initiate a renewed fight for market share among global producers as they attempt to take advantage of the elevated prices while they last, given analysts still expect a surplus to develop this year. WTI futures ended the week down 3.60%.

Bottom Line

While the long-term trend remains bullish for now, some profit taking given the Iran developments is expected with key initial support at $85/barrel in WTI.

Copper

Turning to metals, copper held up surprisingly well last week as futures gained 1.63%. The fact that copper futures did not react in a more negative manner to the Ukraine tensions suggests the conflict is not going to be a bearish game changer for risk assets, at least not yet. The copper market is choppy but trending slightly higher right now and until that changes the industrial metals market will be indicating that the global economic recovery remains healthy.

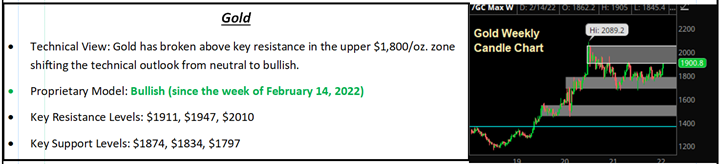

Gold

Gold was the upside standout last week as safe-haven and money flows supported a move to and through $1,900/oz. for the first time since last summer. Gold ended near the highs of the week with a gain of 2.16%. On the charts, gold has broken out and the outlook is now bullish, which is supported fundamentally by a likely continuation of safe-haven flows amid broad market volatility as well as fading real interest rates (also largely linked to volatility and geopolitics).

U.S. Dollar Index

The Dollar Index declined modestly last week as the FOMC minutes weren’t as hawkish as feared while economic data was underwhelming. The Dollar Index fell 0.35%.

In the short term, the Russia/Ukraine situation will continue to cause risk-on/risk-off money flows to impact the currency markets, with risk-off flows causing a dollar rally and risk-on flows pushing the dollar lower. But the larger and more consistent influence over the currency markets is the outlook for future Fed policy, and that didn’t change last week. So, it’s not a surprise the dollar was little changed. The euro and pound both saw mild gains vs. the dollar.

Bottom Line

The Dollar Index in the mid 90’s is appropriate given expected Fed tightening, ECB tightening and BOE tightening, and expectations for that future policy will have to change before we can expect the Dollar Index to sustainably break out or break down from the current mid-90’s trading range.

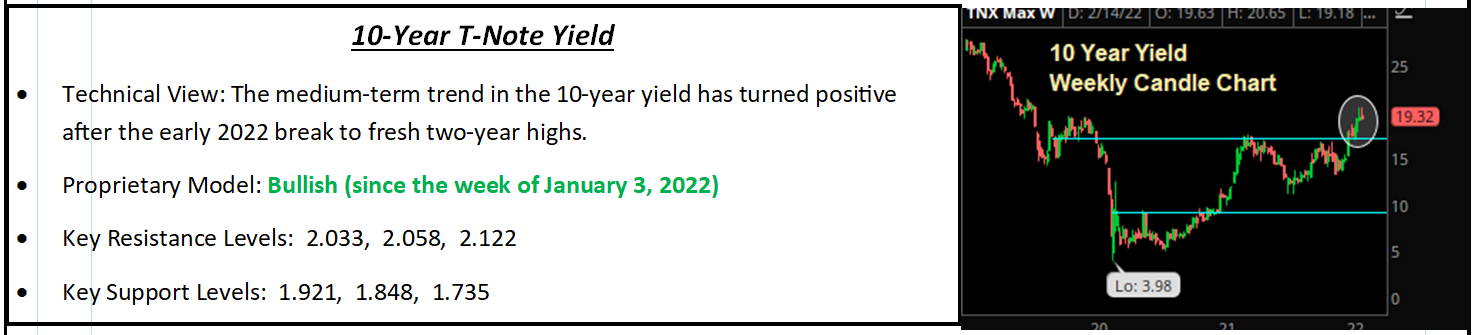

10-Year T-Note Yield

Turning to the 10-year Treasury yield, it declined last week on a combination of risk-off money flows following the deterioration of Russia/Ukraine headlines, combined with the underwhelming economic data and as-expected FOMC minutes. The 10-year yield fell to 1.92%.

The headlines on Russia/Ukraine will continue to cause short-term rallies and declines in the 10-year yield, but the trend remains solidly higher, and barring any major surprises from the Fed, it’s a question of “when” not “if” the 10-year yield trades solidly through 2%.

Regarding the 10s-2s spread, it widened out to 46 basis points this week as the FOMC minutes failed to present any big surprises. Looking forward, the recent lows of 41 basis points are the next support level to watch, although if the Core PCE Price Index is hot this week and growth is underwhelming, we’d expect those lows to be broken, as the trend in 10s-2s is currently towards inversion.

Special Reports and Editorial

Is a Russian Invasion of Donbas a Bearish Game Changer?

One of the most cited reasons stocks dropped last week was because Russia accused Ukraine of shelling Russian rebels in the Ukrainian territory of Donbas, specifically in the Donetsk and Luhansk regions. Those regions are disputed territories, where Russian rebels want to break away from Ukraine, while Ukraine wants to keep the area as part of the country. Here’s why that matters.

In 2014, Russia invaded Georgia to annex Crimea, a region that, like Donbas, was populated by Russians who wanted to break away from Georgia. So, after last week’s accusation by Russia that Ukraine shelled the Russian separatists, analysts believe that Russia may be setting up a precedent to invade Donbas and annex the territory, similar to what happened in Crimea.

So, would that be a materially bearish event? No, not unless it created an all-out war between Ukraine and Russia (which is still unlikely).

Like with Crimea, a Russian invasion of Donbas would result in significant international sanctions against Russia; and those sanctions would put an incremental headwind on U.S. and global growth via potentially higher energy costs and other restrictions. But nothing in those sanctions should materially derail the global economic recovery, assuming there is no further invasion of Ukraine beyond Donbas.

Now, there is the possibility Russia reduces energy exports to Europe, or further invades Ukraine beyond Donbas, but those are significant escalations and it’s safe to say they are not in Russia’s interests. As such, they are not a base-case expectation from markets.

Bottom Line

A limited invasion of Donbas would be a temporary headwind on risk assets, but we would not view that as a bearish game changer unless it spiraled into a broader conflict between Russia and the NATO (which again is unlikely at this point).

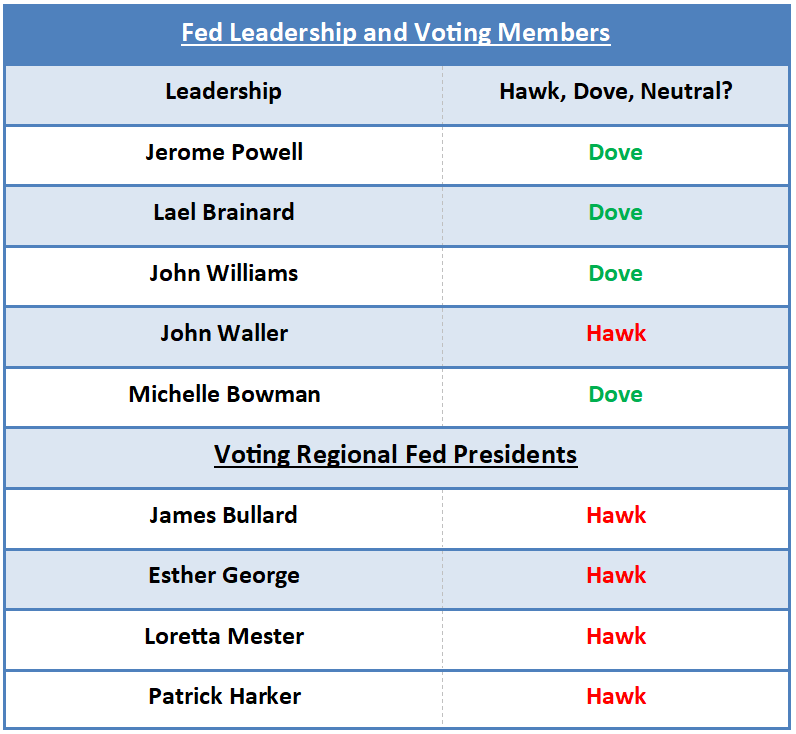

Understanding Fed Hawks vs. Fed Doves

The amount of noise and conflicting commentary coming from the Fed is rapidly increasing, as over the past several days we have had multiple Fed officials openly contracting each other about the future path of policy, and as long as that’s the case, it’s going to lead to more volatility (as we saw last Thursday). Given that reality, we think it’s important that we all understand the relative importance of various Fed speakers, because all Fed commentary is not created equally.

First, for a bit of background on the Fed, only some of the members of the Federal Open Market Committee vote on policy. That means, practically speaking, if a Fed official makes hawkish or dovish commentary that differs from consensus and he or she is not a voting member of the FOMC, we can largely ignore it. From a market standpoint, that means any immediate reaction to those comments (positively or negatively) likely isn’t sustainable (point being, don’t react to it).

For example, San Francisco Fed President Mary Daly made dovish commentary about not wanting to raise rates too quickly. But she is not a voting member of the FOMC this year, so frankly speaking, her dovish commentary isn’t something we should react to as she’s not deciding policy this year.

Second, not all voting members are equal. Fed leadership has historically dictated policy, with the permanent Fed Board members’ opinions carrying much more influence than the regional Federal Reserve Bank heads. Here’s what this means practically for today’s Fed.

First, Powell, Brainard, Williams, Waller and Bowman are Fed Board Members voting this year, so if they make a substantially dovish or hawkish comment, pay attention as that does matter to markets.

Second, if a regional Fed president makes a comment that is out of Fed consensus, even if they are a voting member, then it’s still not likely to produce a sustainable market move unless it’s echoed by Fed leadership (point being, don’t react to it).

Bottom Line

We wanted to provide you with a quick and easy reference to help determine what Fed speak is truly market moving, and what can be generally dismissed, even if there is a short-term reaction. So, in the table below, we’ve listed 1) Fed leadership and 2) Voting members for 2022, so you can quickly and easily identify if a Fed comment is coming from a potentially market-moving Fed member, or just someone voicing an opinion that can’t actually vote this year.

Looking forward, there are three takeaways from this Fed reality.

First, if markets move because of commentary from any of the people in this table, that’s a legitimate move and while it might not signal a change in Fed policy, it needs to be respected as they are all voting members of the FOMC this year (so Bullard’s comments rightly caused volatility last week, especially given valuations).

Second, the higher the name on this list, the more important and impactful the commentary is. That makes Powell and Brainard the two most important Fed voices, but Williams, Waller and Bowman are also important. Regional Fed Presidents Bullard, George, Mester and Harker will carry the least weight.

Finally, if a Fed official is not on this list, then it’s unlikely their commentary, regardless of how hawkish or dovish, will produce a sustainable move in markets.

Bottom Line

Over the past 36 hours we’ve had three Fed officials make comments, and two were hawkish (George and Bullard) and one was dovish (Daly). We can expect that type of variance going forward, but this table will help us cut through that noise and know, right away, if a Fed comment is really something that could sustainably move markets, or if it’s just generated a short-term trading reaction. I am going to print out this table and tape it to my desk so I can use it as a quick reference for Fed commentary, and I’d encourage you to do the same.

Fed Wildcard: Appointments

You may have read over the past couple of months about the topic of Fed appointments, and I want to explain why that matters to markets.

Normally, there are 12 voting members on the FOMC. That consists of seven Federal Reserve Board members (who are permanently on the board), the New York Fed President (who is always a voting member) and a rotation of four of the regional Fed presidents.

Because of a delay in confirmation of Fed Board members by the Senate, there are currently only five Fed governors, so there are only 10 Fed officials voting instead of 12 going forward. That will change later this year as the Senate confirms these officials, but the bottom line is that those appointments could change the relative “hawk/dove” mix at the Fed, although it’s too early to tell by how much. As those appointments take hold, we’ll update this table accordingly and make sure you know the new names to watch, because “Fed watching” will remain the primary “sport” for investors this year, and especially so in the coming months (until we have clarity on rate hikes and balance sheet reduction).

FOMC Minutes Takeaways

The minutes from the January meeting were no more hawkish than feared.

On an absolute basis, the commentary in the FOMC minutes from the January meeting were hawkish, as there was extensive debate on the pace of rate hikes and balance sheet reduction. But in partial testament to how far the Fed has moved market expectations, nothing in the minutes was more hawkish than markets were currently expecting, and as a result it created a “sell the rumor/buy the news” reaction that saw stocks rally.

The minutes showed there was broad consensus among the FOMC that rates needed to move up more quickly than during the previous 2015-2018 rate hike cycle, but that’s not a surprise. More directly, there was no clarification on whether we get a 50-bps hike or a 25-bps hike in March. So, the minutes only confirmed what we know already, that the Fed will hike multiple times this year—but it didn’t give us clarity into the next key question on rates: 25 or 50 bps in March?

Regarding the balance sheet, it was a mild surprise that “some” FOMC members wanted to end QE at the January meeting (vs. the stated end of March), but “some” is a minority and as such that didn’t move markets.

Regarding the plan for Quantitate Tightening, not much was revealed. Broadly, FOMC members agreed that the balance sheet would need to be reduced more quickly than during the previous cycle (but that’s not hard, last time balance sheet reduction was very gradual), but beyond that they gave no insight into when QT would begin. Additionally, they also admitted it was unclear how much QT should occur. So, again, while it was “hawkish,” the FOMC openly discussed balance sheet reduction, we already knew they were discussing it from the December minutes, and the minutes didn’t reveal anything new.

The market was braced for more hawkish FOMC minutes, so when they failed to reveal anything “new” on the hawkish front, it caused a mild reflex rally in stocks that saw the S&P 500 erase earlier losses and turn modestly positive.

Bottom Line

The Fed is hawkish, they are raising rates starting in March, and Quantitative Tightening will begin in the summer (sometime between June and August). But the minutes provided no additional clarity to the two current Fed questions: Will the Fed hike 25 or 50 bps in March? How quickly will the Fed reduce the balance sheet? Those answers will determine whether the Fed is viewed as more hawkish (and that would hit stocks) or not as hawkish (which would spark a rally). For now, we’ll have to wait until there’s more clarity either from Fed speeches between now and the March 16 meeting, or from the meeting itself.

Oil Market Update

Weekly EIA Data and Oil Market Update

The weekly EIA report was a very mixed bag. On the headlines, commercial crude oil stockpiles rose by +1.1MM bbls vs. (E) -600K (API: -1.1MM) last week, which was dually bearish, albeit only modestly so, while gasoline stocks dropped by -1.3MM bbls vs. (E) +500K (API -900K) and distillate inventories fell -1.6MM vs. (E) -1.7MM (API: -500K), both of which were slightly bullish. Inventories at the major oil hub in Cushing, OK, however, extended a recent decline for a sixth consecutive week with another -1.9MM bbls to just 25.8MM last week. This development compounded fears that supply levels at Cushing are fast approaching an operational minimum, which could cause reverberating issues across the physical oil market.

Other details in the release were less bullish and suggest that a rebound in Cushing inventories could trigger a profit-taking pullback in an otherwise still-upward-trending market as implied consumer demand for gasoline fell back by -556K b/d to 8.570MM, ending a multi-week, post-Omicron rebound. Additionally, refinery runs fell by -2.9% to 85.3% vs. (E) 87.5% suggesting a diminishing market outlook by downstream traders. Adverse weather on the Gulf Coast was cited as a reason for the drop-off in refining activity but we will want to see that confirmed by a rebound in the utilization rate in the coming weeks. Finally, domestic production remained anchored at 11.6MM b/d, which shows limited interest by U.S. producers to ramp up production in the current environment, despite higher prices (slightly bullish).

Late in the day, after the Nymex close, a headline crossed the wires that Iran’s Senior Nuclear Negotiator, Ali Bagheri Kani, stated that the U.S. and Iran are “closer than ever to an agreement” in resurrecting the 2015 nuclear deal. The prospect that somewhere between 500K and 1MM b/d of supply could come back to the global market, relatively quickly, hit futures hard and both benchmarks fell to session lows in after-hours trade last Wednesday.

Bottom Line

Near-term supply dynamics in the U.S., namely inventories at Cushing, have been propping up the oil market recently while demand metrics have been generally strong. But implied consumer demand in the EIA report showed a drop off in demand, and that paired with the bearish Iran headlines late in the day, initiated a profit-taking pullback in oil that brought WTI back down to trade with a $90 handle. Looking ahead, an Iran nuclear deal is a potential game changer for the market but not necessarily a bearish one right away but rather one that would shift the outlook from decidedly bullish to neutral. If this scenario were to play out, we would expect to see WTI trade between $85 and $95/barrel while if talks fall through, a run towards our longer-term upside target of $105 would remain intact.

By Vann Equity Management